You graduated, landed a job, and suddenly you're staring at bills, student loans, and a paycheck that disappears faster than expected. Most schools never teach you how to actually manage money day to day, and that gap is real. Core personal finance modules cover everything from banking basics to credit building and debt management, yet most young adults still feel underprepared. This guide walks you through the essentials in plain language, from setting up your first budget to building credit safely, all while keeping your personal data where it belongs: with you.

Table of Contents

- Laying the groundwork: What you need before you start

- Building a budget: Step-by-step for young adults

- Saving and building credit: Turning habits into progress

- Troubleshooting and staying on track: Adjusting for real life

- Why most guides miss: Privacy, flexibility, and real growth

- Move from learning to action: Tools for next-level finance

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Know your basics | Master banking, budgeting, and tracking before moving to advanced topics. |

| Pick the right budget | Choose a budget rule that fits your income and lifestyle, and adjust as needed. |

| Automate savings and credit | Set up automatic transfers and payments for steady progress with minimal effort. |

| Adapt to real life | Review and adjust your financial plan regularly as your circumstances change. |

Laying the groundwork: What you need before you start

Before you open a spreadsheet or download any app, you need to understand what personal finance actually covers. It is not just budgeting. Think of it as a set of modules you build on over time, each one supporting the next.

Core personal finance modules for young adults include banking basics, goal setting, income tracking, budgeting, saving, credit building, borrowing, debt management, insurance, and life transitions. That is a lot, but you do not tackle everything at once. You start with the foundation and layer skills as your situation grows.

Here is a quick overview of the key modules and roughly how long each takes to get comfortable with:

| Module | What it covers | Recommended time |

|---|---|---|

| Banking basics | Accounts, fees, direct deposit | 1 week |

| Goal setting | Short and long-term targets | 2 to 3 days |

| Income tracking | All income sources, net vs. gross | 1 week |

| Budgeting | Spending categories, rules | 2 weeks |

| Saving | Emergency fund, automation | Ongoing |

| Credit building | Score, cards, reports | 1 month |

| Debt management | Loans, payoff strategies | Ongoing |

| Insurance | Health, renter's, auto basics | 1 week |

Why does this sequence matter? Because skipping ahead, say, jumping to investing before you have an emergency fund, creates fragile financial habits. Each module builds real confidence before you move forward.

When it comes to tools, privacy matters from day one. Many free apps monetize your financial data. Look for beginner finance skills platforms that are transparent about what they collect and why. Ideally, choose tools that store data locally on your device or use end-to-end encryption.

Key habits to build early:

- Track every income source, including side gigs and irregular payments

- Separate your accounts: one for bills, one for spending, one for saving

- Set at least one specific financial goal before you build a budget

- Review your bank statements weekly, not monthly

Pro Tip: Create a single secure folder or app on your phone dedicated to financial info. Keep account numbers, login hints (not passwords), and your monthly income summary there. It sounds simple, but having everything in one private place removes the friction that causes most people to fall off track.

Building a budget: Step-by-step for young adults

With your basics in place, it is time to create a budget that fits your lifestyle and goals. The most well-known starting point is the 50/30/20 rule.

The 50/30/20 rule allocates 50% of your after-tax income to needs, 30% to wants, and 20% to saving or debt repayment. It is clean, easy to remember, and works well if your income is stable and your cost of living is moderate.

But it is not the only option. Alternative rules like 60/30/10 or 70/20/10 suit high-cost cities or aggressive savings goals better. Here is a comparison:

| Budgeting method | Needs | Wants | Savings/Debt | Best for |

|---|---|---|---|---|

| 50/30/20 | 50% | 30% | 20% | Stable income, moderate cost of living |

| 60/30/10 | 60% | 30% | 10% | High rent or essential expenses |

| 70/20/10 | 70% | 20% | 10% | Entry-level salaries or variable income |

None of these rules are laws. They are frameworks. The goal is to get a working system running, then refine it.

Here is how to set up your first budget in four steps:

- Choose your method. Pick 50/30/20 if you are unsure. You can always switch.

- Gather your data. Pull 30 days of bank and card statements. Add up your real income and real spending by category.

- Build your plan. Assign each dollar a job using your chosen percentages. Be honest about what counts as a "need" versus a "want."

- Track and review. Check in weekly. After one month, compare your plan to what actually happened.

Privacy note: if you use budgeting apps, read the privacy policy before connecting your bank account. Many popular apps sell anonymized transaction data to third parties. Look for apps that offer manual entry or local storage options.

Pro Tip: Before you lock in any budget rule, track your actual cash flow for one full month without changing anything. Most people are surprised by where their money actually goes, and that data is far more useful than any estimate.

Saving and building credit: Turning habits into progress

Once you have a spending plan, the next step is making financial progress on savings and credit. These two areas work together more than most people realize.

Building an emergency fund of 3 to 6 months' expenses and establishing credit early sets the foundation for long-term financial confidence. Start small. Even $500 in a dedicated savings account changes your relationship with unexpected costs.

Steps to build both at the same time:

- Open a separate savings account labeled "emergency fund" and automate a fixed transfer on payday

- Apply for a secured credit card with a low limit, ideally $300 to $500

- Pay the full balance every month, not just the minimum

- Set up automatic payments so you never miss a due date

- Check your credit report every few months using a secure, privacy-respecting tool

- Avoid opening multiple credit accounts in a short period, as each hard inquiry temporarily lowers your score

Compound interest is often called the eighth wonder of the world. Starting to save even $50 a month at age 22 instead of 32 can result in tens of thousands of dollars more by retirement, simply because of the extra decade of growth.

When choosing credit-building apps, look for tools that do not require you to hand over your Social Security number or full banking credentials just to monitor your progress. Some apps offer credit score tracking with minimal data sharing, which is a much safer approach for beginners.

The behavioral side matters too. Automating your savings and credit payments removes the decision from your daily routine. You do not have to rely on willpower. The system does the work.

Pro Tip: Set up two automatic transfers on payday: one to your emergency fund and one to cover your minimum credit card payment. Do this before you spend anything else. It takes ten minutes to set up and protects you from the two most common early financial mistakes.

Troubleshooting and staying on track: Adjusting for real life

Even the best plans run into challenges, but with the right approach you can adapt and keep improving. Life changes fast, especially in your twenties, and your budget needs to keep up.

The 50/30/20 rule can be too rigid for gig workers or anyone with volatile income. Flexibility and regular adjustment are not optional extras. They are part of the system.

What to do when your budget stops working:

- Identify the leak. Pull your last 30 days of transactions and find the category that went over. One category usually causes the cascade.

- Recategorize honestly. Sometimes what you labeled a "want" is now a "need" because your life changed. Adjust the labels before adjusting the numbers.

- Switch your method temporarily. If your income dropped, move to 70/20/10 for one or two months without guilt. The goal is sustainability, not perfection.

- Rebuild your baseline. After a major change like a new job, a move, or a big expense, redo your income and expense audit from scratch.

Common mistakes that derail young adults:

- Not tracking spending for even one week per month

- Using finance apps without checking their data collection policies

- Skipping the automation step and relying on manual transfers

- Ignoring small recurring charges that quietly drain accounts

Quick fixes you can apply today:

- Cancel one subscription you have not used in 60 days

- Set a weekly five-minute calendar reminder to review your spending

- Move your emergency fund to a separate bank so it is harder to access impulsively

Without an emergency fund, a single unexpected expense, like a car repair or a medical bill, can unravel months of careful budgeting. Regular reviews and a funded safety net are your best defense.

When adapting your budget, the most important thing is to keep the habit alive even when the numbers change. A rough budget you actually use beats a perfect one you abandon.

Why most guides miss: Privacy, flexibility, and real growth

Here is something most personal finance content will not tell you: the rules are not the hard part. The hard part is building a system that fits your actual life, not the life a financial planner imagined for you.

Most guides focus on formulas and ignore two things that matter enormously right now. First, privacy. When you connect your bank to a free app, you are often paying with your data. That is a real cost, and most guides treat it as a footnote. Privacy-focused finance tools exist, and choosing them is a financial decision, not just a tech preference.

Second, flexibility. The gig economy, remote work, and career pivots mean that many young adults have income that looks nothing like a traditional paycheck. A rigid rule applied to irregular income creates frustration, not progress.

The deeper issue is mindset. Real financial growth is not about following a rule perfectly for one month. It is about building habits that survive job changes, relationship changes, and the general chaos of your twenties. That requires a framework you can adjust, tools you trust, and a willingness to review and reset without shame. The guides that skip this part are the ones that leave you feeling like you failed, when really the advice just did not fit.

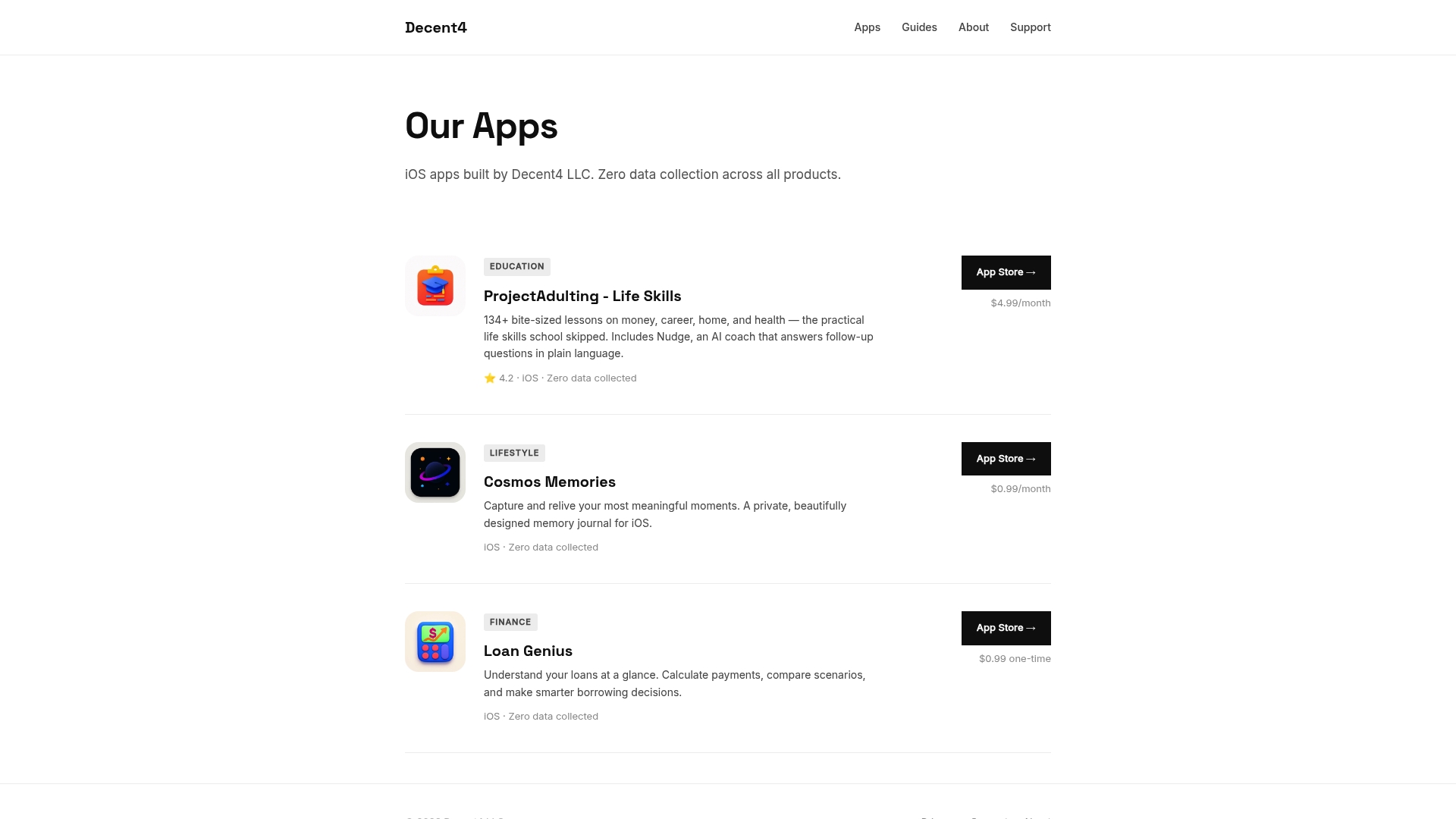

Move from learning to action: Tools for next-level finance

Ready to turn insight into action? The gap between knowing and doing is where most financial progress stalls, and the right tools close that gap fast.

The Decent4 app suite is built specifically for young adults who want practical skills without sacrificing privacy. Every app in the lineup operates on a zero data collection model, so your financial information stays yours. The ProjectAdulting initiative takes this further with over 134 AI-guided lessons covering budgeting, credit, career planning, and more, all delivered in short, actionable formats that fit a busy schedule. If you are ready to move from reading about money management to actually practicing it, this is the logical next step.

Frequently asked questions

What is the 50/30/20 budgeting rule and how do I use it?

The 50/30/20 rule splits your after-tax income into 50% for needs, 30% for wants, and 20% for savings or debt repayment. Total your monthly take-home pay and assign each percentage to the matching spending category.

How can I build credit safely as a young adult?

Start with a secured credit card, pay the full balance on time every month, and keep your balance well below the credit limit. Use a secure, privacy-respecting app to monitor your score without exposing sensitive data.

Which budgeting method is best if my income changes a lot?

Flexible rules like 70/20/10 or regular monthly budget reviews work better for gig workers or anyone with variable pay than a fixed percentage system.

How much should I save for emergencies?

Aim for an emergency fund covering 3 to 6 months of essential living expenses, and build it gradually with small, automated transfers that happen before you spend anything else.